❓ Can zero-knowledge proofs bridge the gap between KYC compliance and anonymity?

-

Answer:

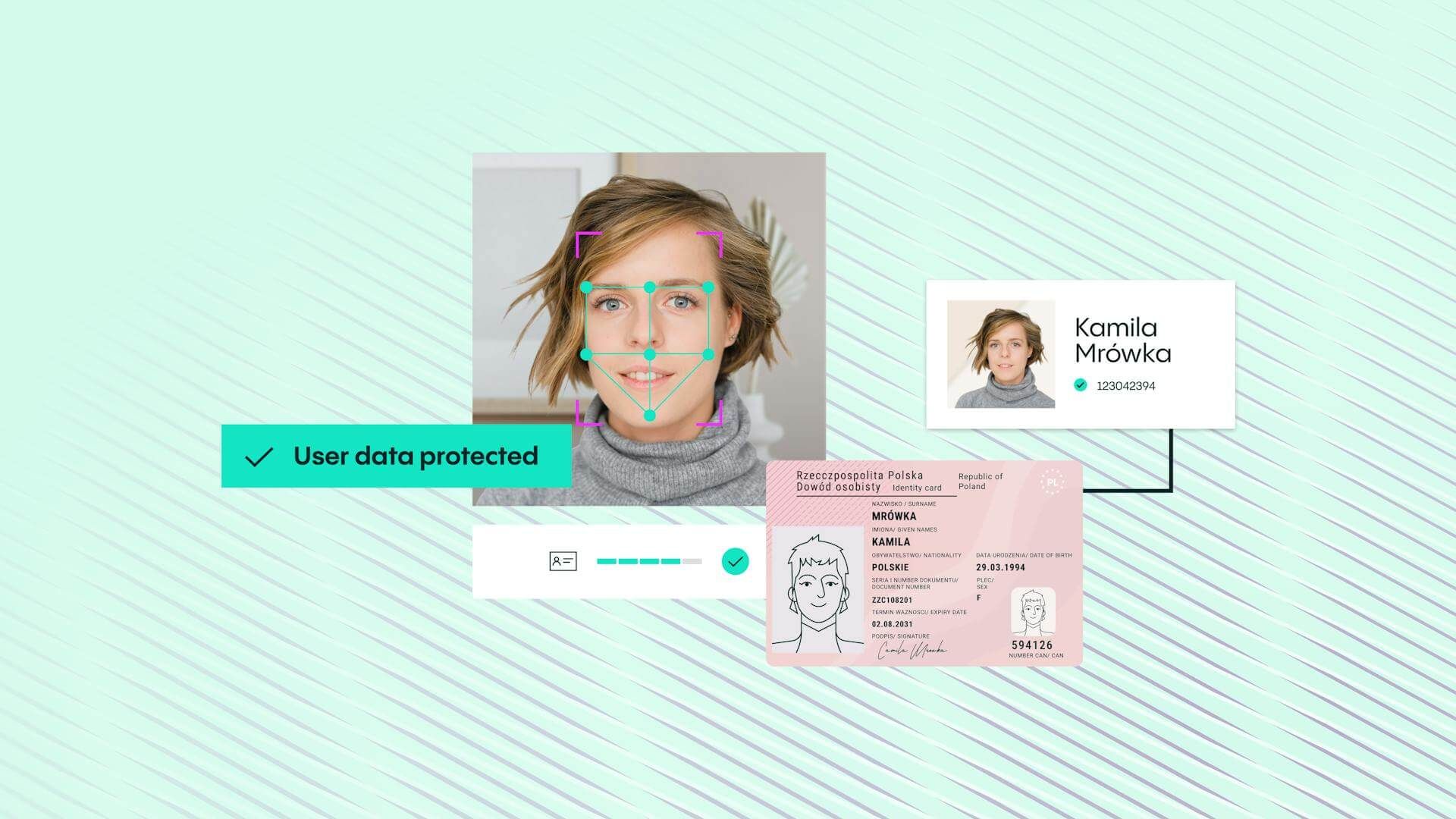

Yes — in theory, and increasingly in practice.Current problem: Compliance demands “prove you’re not laundering,” while crypto natives demand “don’t dox me.” Traditional KYC solutions break privacy by design.

ZK solution: A user can prove “I’m over 18,” “I’m not sanctioned,” or “I passed KYC with a licensed provider” without revealing their name, address, or documents. This is what projects like zkKYC and Polygon ID are building.

Adoption hurdles:

Regulators don’t yet fully trust math > paper.

ZK systems need a network of trusted issuers (banks, notaries, identity providers) to issue those attestations.

Interoperability matters — different chains and apps need to agree on the proof standards.

Real-world catalyst: EU’s digital identity framework (EUDI Wallet) and UK/US experiments in privacy-preserving AML could make zkKYC the default bridge between compliance and crypto-native anonymity.

TL;DR: Zero-knowledge proofs won’t eliminate regulation, but they might rewrite it — turning KYC from “give me everything” into “prove only what’s needed.”

TL;DR: Zero-knowledge proofs won’t eliminate regulation, but they might rewrite it — turning KYC from “give me everything” into “prove only what’s needed.” -

Yes — in theory, and increasingly in practice.

The current issue is a clash of cultures: compliance says “prove you’re not laundering,” while crypto natives say “don’t dox me.” Traditional KYC solves one but completely breaks the other.

That’s where ZK proofs shine. Instead of handing over your name, address, and passport, you can just prove specific facts like:

“I’m over 18.”

“I’m not on a sanctions list.”

“I passed KYC with a licensed provider.”

…all without revealing the underlying documents. This is what zkKYC and Polygon ID are already experimenting with.

-

Biggest hurdles right now:

Regulators still trust paper over math.

ZK systems need trusted issuers (banks, notaries, ID providers) to vouch for the data.

Proofs have to be interoperable across chains/apps — otherwise every project reinvents the wheel.

Why it matters soon: frameworks like the EU’s EUDI Wallet and UK/US pilots in privacy-preserving AML could normalize zkKYC. That would turn compliance from “give me everything” into “prove only what’s relevant.”

TL;DR: ZK won’t erase regulation, but it might rewrite it — making KYC less invasive while still satisfying compliance.