🔍 FTX Customers Now Say Law Firm Was “Central” to the Fraud — New Evidence Emerges

-

The FTX collapse is back in the headlines — but this time, the spotlight isn’t on Sam Bankman-Fried. It’s on one of his former law firms.

The Accusation:

The Accusation:

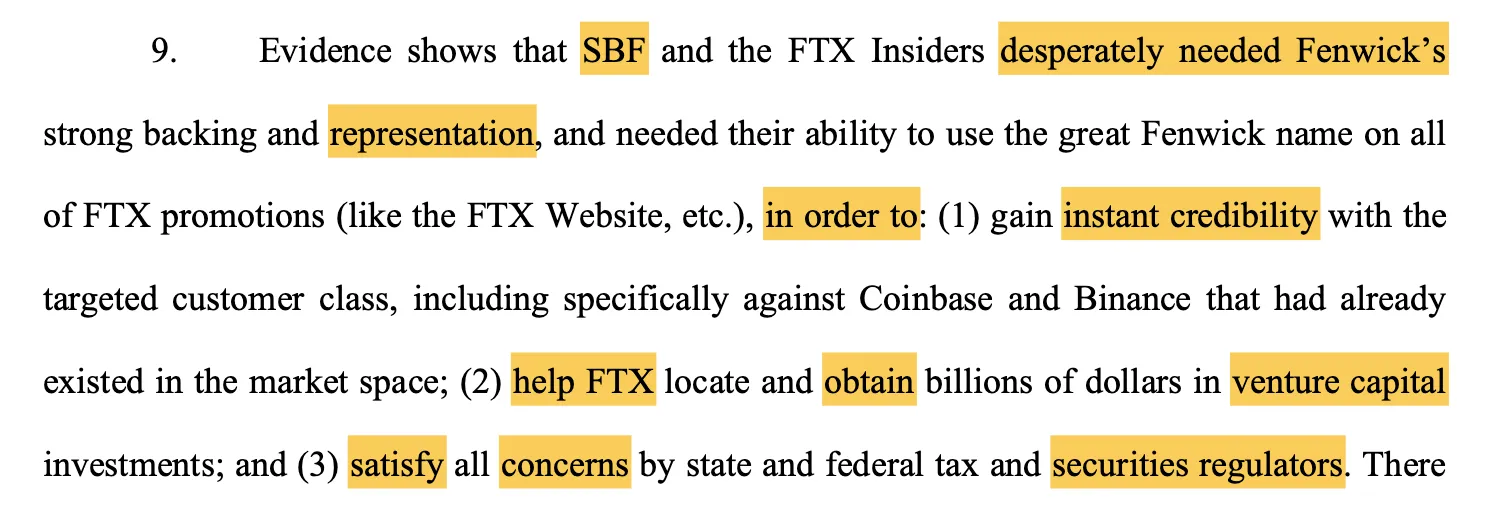

FTX customers have moved to update their lawsuit against Fenwick & West, claiming fresh evidence from SBF’s criminal trial and bankruptcy investigations shows the firm was deeply involved in building the structures that made the fraud possible.Key allegations include:

Designing and approving “conflicted companies” like Alameda Research and North Dimension with zero safeguards to protect billions in customer funds. Advising on how to hide misuse of customer money, according to testimony from former execs Nishad Singh, Gary Wang, and Caroline Ellison. Creating shell entities to obscure asset flows and implementing auto-deleting Signal messages for executives. Facilitating intercompany transactions that misused customer assets. From the courtroom:

From the courtroom:

An independent examiner in the FTX bankruptcy reportedly reviewed 200,000+ internal documents and concluded Fenwick was “deeply intertwined” in nearly every aspect of FTX’s misconduct. The Securities Angle:

The Securities Angle:

The updated complaint adds two new securities law claims (Florida & California), accusing Fenwick of helping design, market, and facilitate the sale of FTT tokens, yield accounts, and other unregistered investment products. ️ Fenwick’s defense?

️ Fenwick’s defense?

They’ve previously argued a law firm can’t be held responsible for a client’s wrongdoing if the actions were within the scope of legal representation. Investor takeaway:

Investor takeaway:This case isn’t just about crypto — it’s about whether top-tier law firms could face real legal and financial risk for enabling questionable client conduct. If the court accepts these new claims, it could set precedent for lawsuits against professional service providers tied to major financial scandals. Watch for potential ripple effects in legal risk premiums for firms advising high-growth but high-risk ventures.